//+------------------------------------------------------------------+

//| LaguerreFilter.mq4 |

//| |

//| Laguerre Filter |

//| |

//| Algorithm taken from book |

//| "Cybernetics Analysis for Stock and Futures" |

//| by John F. Ehlers |

//| |

//| contact@mqlsoft.com |

//| http://www.mqlsoft.com/ |

//+------------------------------------------------------------------+

#property copyright "Coded by Witold Wozniak"

#property link "www.mqlsoft.com"

#property indicator_chart_window

#property indicator_buffers 2

#property indicator_color1 Red

#property indicator_color2 Blue

extern double Gamma = 0.8;

double Filter[];

double FIR[];

double L0[];

double L1[];

double L2[];

double L3[];

int buffers = 0;

int drawBegin = 0;

int init() {

drawBegin = 4;

initBuffer(Filter, "Laguerre Filter", DRAW_LINE);

initBuffer(FIR, "FIR", DRAW_LINE);

initBuffer(L0);

initBuffer(L1);

initBuffer(L2);

initBuffer(L3);

IndicatorBuffers(buffers);

IndicatorShortName("Laguerre Filter [" + DoubleToStr(Gamma, 2) + "]");

return (0);

}

int start() {

if (Bars <= drawBegin) return (0);

int countedBars = IndicatorCounted();

if (countedBars < 0) return (-1);

if (countedBars > 0) countedBars--;

int s, limit = Bars - countedBars - 1;

for (s = limit; s >= 0; s--) {

L0[s] = (1.0 - Gamma) * P(s) + Gamma * L0[s + 1];

L1[s] = -Gamma * L0[s] + L0[s + 1] + Gamma * L1[s + 1];

L2[s] = -Gamma * L1[s] + L1[s + 1] + Gamma * L2[s + 1];

L3[s] = -Gamma * L2[s] + L2[s + 1] + Gamma * L3[s + 1];

Filter[s] = (L0[s] + 2.0 * L1[s] + 2.0 * L2[s] + L3[s]) / 6.0;

FIR[s] = (P(s) + 2.0 * P(s + 1) + 2.0 * P(s + 2) + P(s + 3)) / 6.0;

if (s > Bars - 4) {

L0[s] = P(s);

L1[s] = P(s);

L2[s] = P(s);

L3[s] = P(s);

Filter[s] = P(s);

}

}

return (0);

}

double P(int index) {

return ((High[index] + Low[index]) / 2.0);

}

void initBuffer(double array[], string label = "", int type = DRAW_NONE, int arrow = 0, int style = EMPTY, int width = EMPTY, color clr = CLR_NONE) {

SetIndexBuffer(buffers, array);

SetIndexLabel(buffers, label);

SetIndexEmptyValue(buffers, EMPTY_VALUE);

SetIndexDrawBegin(buffers, drawBegin);

SetIndexShift(buffers, 0);

SetIndexStyle(buffers, type, style, width);

SetIndexArrow(buffers, arrow);

buffers++;

}

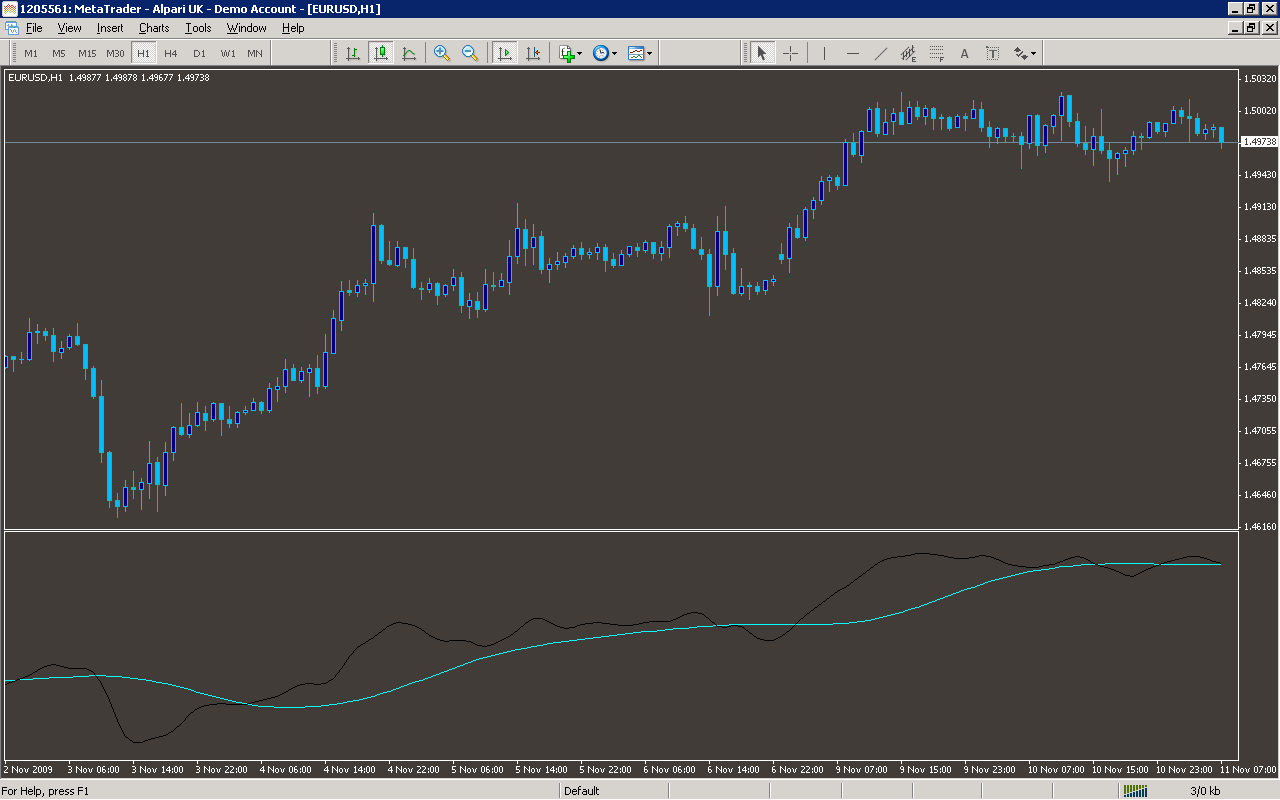

Sample

Analysis

Market Information Used:

Series array that contains the highest prices of each bar

Series array that contains the lowest prices of each bar

Indicator Curves created:

Implements a curve of type type

Indicators Used:

Custom Indicators Used:

Order Management characteristics:

Other Features: